Patrick A. Pintus, Yi Wen, Xiaochuan Xing, 2022, European Economic Review, Volume 148, 104219

»

Credit supply goes up by more than credit demand during expansions,

so that the interest rate goes down and a boom follows.

Virtually all US firms rely on some form of borrowing to finance productive investment, working capital and other types of expenses. For example, corporate firms issue bonds while non-corporate companies rely to a large extent on bank loans. A striking feature is that the real interest rate paid by US firms is countercyclical: typically low during expansions but tending to rise during recessions.

Such a property has far-reaching macroeconomic consequences: when the borrowing cost is low, investment financing by firms is cheaper and the economy booms. This is confirmed by impulse responses obtained from a vector autoregressive model, which show that all variables are procyclical, i.e. they move hand in hand with output, except for the debtor interest rate. When investment booms, the interest rate stays below trend for several quarters. This suggests that during expansion periods, the willingness of creditors to extend credit rises so much that, despite an increase in credit demand, the cost of credit goes down.

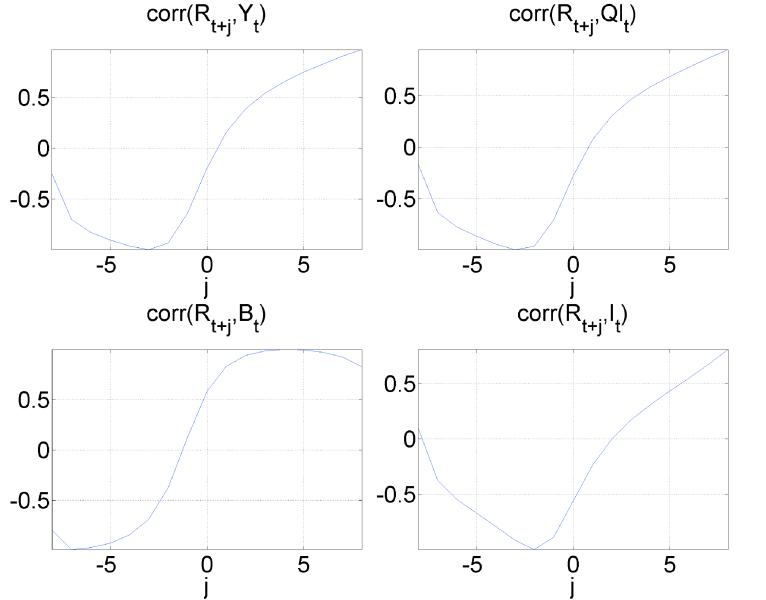

Correlations between the interest rate at various leads and lags (in quarters) and macroeconomic variables are reported in Figure 1.

Figure 1. Empirical lead-lag correlations - up to 8 quarters - of the real interest rate (denoted R), with output (Y), land price (Ql), debt (B),and investment (I),

based on US data from 1975 to 2010.bands in red).

A notable feature of Figure 1 is the so-called inverted leading indicator property of the interest rate: the lead-lag correlations all have an S-shaped pattern. The correlations of the interest rate 5 quarters ago with current values for output and other variables are negative in Figure 1. This means that a low interest rate 5 quarters ago is associated with a boom in activity today: cheap debt then accumulates and finances a boom later on. Further, a high level of output today will be accompanied by a higher interest rate 5 quarters down the road: as the economy reverts back to its trend, the interest rate tends to rise.

The inverted leading indicator property of the borrowing cost is a long-standing puzzle. Standard business cycle models do not accord with it: high investment and output are associated with a high interest rate in such settings. We tackle this puzzle by introducing a credit market that channels funds from lenders to borrowers into the textbook business-cycle setting. Our analysis relies on the interaction of two main features. First, due to collateral constraints to the Kiyotaki and Moore, a credit market friction creates a wedge between credit supply and credit demand. Second, we relax an assumption that is often implicit in the existing literature: loans are such that the interest rate is not set when the loan is negotiated, but instead is state-contingent and responds to changes in aggregate economic conditions when the loan repayment is due. This is the case when, for example, firms borrow at a variable interest rate.

Both the demand for and the supply of credit then go up during booms. On the demand side, firms that rely on variable-rate loans decide to borrow and invest more when they expect interest rates to go down. In the absence of any change in credit supply, this would push up the interest rate. But when the collateral channel operates on the supply side of the credit market, this conclusion can be reversed: to the extent that the market value of collateral is larger during booms, lenders are happy to lend more. Evidence of such a collateral channel has received strong support from the empirical micro literature, which shows that a large fraction of US firms hold real estate and use it as collateral to borrow more and finance their investment.

In the realistic case where loan-to-value ratios are smaller than one, credit supply goes up by more than credit demand during expansions, so that the interest rate goes down and a boom follows. Provided that the rise in the market value of collateral - e.g. land price - is persistent, the boom is persistent as well. In other words, the interest rate inherits the inverted leading indicator property. To sum up, collateralizable assets - most notably real estate - flow from lenders to borrowers while debt repayments from the latter to the former go down during expansions: a redistribution channel operates in favour of borrowers.

To gauge the empirical bite of such a redistribution channel, a medium-sized model is estimated using US data from 1975 to 2010. Two settings are compared: (i) one with loans that have predetermined repayments - that is, fixed interest rates – (ii) an extended one with variable-rate loans. In addition, in the latter setting, redistribution shocks that are purely expectation-driven can materialise, whereby borrowers change their views about the level of the real interest rate that they expect to repay in later periods.

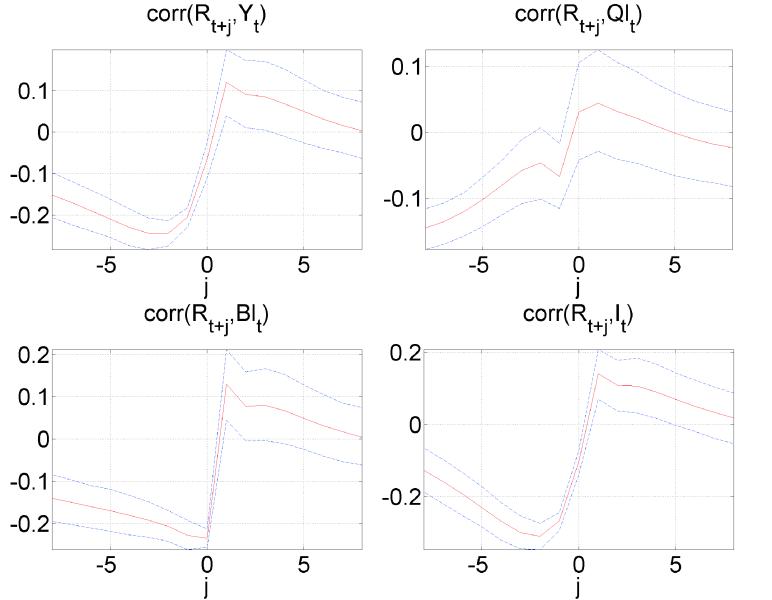

Two lessons can be drawn from the outcome of the estimation procedure. First, only the model with a significant proportion of variable-rate loans in the economy delivers the inverted leading indicator property. This can be seen from Figure 2, which is the theoretical analogue of Figure 1.

Figure 2. Theoretical lead-lag correlations - up to 8 quarters - of the real interest rate (denoted R), with output (Y), land price (Ql), debt (B), and investment (I),

based on US data from 1975 to 2010 (95% confidence bands in red).

Second, the estimated model can also be used to measure the empirical importance of expectational shocks to the interest rate and they turn out to matter. For example, they account for about 30% of output volatility after eight quarters, and close to 50% after sixteen quarters. Similarly, expectation shocks explain a large chunk of the variances of consumption, investment, credit, hours worked, wages, and, to a lesser extent, land price.

Although this analysis makes a useful contribution by showing that the redistribution channel matters empirically, it still has several shortcomings. Most importantly, it is silent on the mechanisms at the origin of such redistribution shocks; in particular since it focuses on a setting in which all magnitudes are real, not nominal. An obvious candidate is monetary policy, as most contracts serving as credit market instruments are: (i) denominated in nominal terms, and (ii) subject to inflation risk even at short horizons. Although the literature has already pointed to such a mechanism, it has not yet been able to rationalise the inverted leading indicator property of the interest rate in a nominal environment. Such a challenge should therefore be addressed in future research and would deliver precious information about the transmission of monetary policy.

→ This article was issued in AMSE Newletter, Winter 2023.

© Zoe / Adobe Stock